A co-investment is a direct investment made alongside a general partner into a specific deal, outside the main fund. For a family office, it means putting capital into an individual company or asset on terms negotiated for that transaction, rather than committing to a blind pool. The structure is appealing because it can reduce or eliminate management fees and carried interest, and because it gives the family office more visibility into exactly where its money is going.

The appetite is real and growing. PwC reported that 60 percent of family office investments in the first half of 2024 involved co-investments with other investors, and Citi’s 2024 survey found that three quarters of family offices now engage in some form of direct investing, with co-investments serving as one of the primary ways they do it at scale.

But the operational reality of co-investments looks very different from the deal itself. Each co-investment brings its own capital call schedule, its own distribution notices, its own reporting format, and its own set of tax documents. None of that arrives in a standardized way. The GP sends what the GP sends, and the family office back office is left to reconcile it. As co-investment activity grows, so does the volume of unstructured documents that need to be rekeyed, normalized, and tied back to the books before anything useful can be reported or audited.

Co-investments in practice

Most family offices encounter co-investments through an existing GP relationship. A manager sees a deal that needs more equity than the fund alone can provide, or wants to deepen a relationship with a valued LP, and offers the family office a chance to invest directly alongside the fund. The family office evaluates the opportunity, cF:ommits capital, and participates in the economics of that specific transaction.

The appeal is understandable. Co-investments give family offices concentrated exposure to individual deals they can diligence themselves, rather than relying entirely on a GP’s discretion across a pooled vehicle. They often come with reduced or no management fee and carried interest, which over time can meaningfully improve net returns. Hamilton Lane describes this fee advantage as a common feature of co-investment programs, though it also notes the concentration risk and operational workload that come with it. For offices trying to deploy large amounts of capital efficiently, co-investments offer a way to put more money to work in higher-conviction positions without paying full blind-pool economics on every dollar.

What gets less attention is what happens after the commitment is made. The deal closes, and then the documents start arriving. Capital call notices come on the GP’s schedule. Distribution notices follow their own timeline. Quarterly statements, capital account summaries, and annual tax documents like K-1s show up across portals, emails, and occasionally still by mail. Each GP formats these documents differently. Some send clean PDFs with consistent layouts. Others send scanned images or Excel attachments with varying column structures and terminology.

The family office back office has to take all of that and turn it into something that can be posted to the general ledger, reflected accurately in portfolio reporting, and supported in an audit. That means reading each document, extracting the relevant figures, matching them against existing records, and entering them into whatever system the office uses for accounting and performance tracking. For a single co-investment with one GP, this is manageable. For a program with ten or twenty active co-investments across several managers, it becomes a recurring data handling problem that competes for the same staff time as everything else the office needs to close each quarter.

BNY Wealth’s 2025 family office study identified understaffing as a key constraint on direct investing programs, and co-investments are a direct contributor to that pressure. The bottleneck is rarely the investment decision. It is the operational overhead of keeping the data clean, current, and auditable after the decision has already been made.

Why co-investments stress back office workflows

The operational weight of co-investments sits almost entirely in the documents. Every co-investment generates its own stream of GP notices, capital account statements, distribution schedules, and tax filings. These are the primary inputs to accounting and reporting, and they arrive as PDFs, portal downloads, email attachments, and occasionally scanned images. There is no standard format. There is no shared schema. The family office receives whatever each GP produces, and the back office has to work with it.

The inconsistency runs deeper than layout. One GP’s capital call notice might label a field “unfunded commitment.” Another calls it “remaining commitment” or “uncalled capital.” Distribution notices vary in how they break out return of capital, gains, income, and fee offsets. Quarterly statements differ in what they include, how they calculate performance, and whether they report on a gross or net basis. The terminology is close enough to look interchangeable but different enough to cause posting errors if someone processes it on autopilot. Every document requires a careful read, and that careful read takes time that scales linearly with the number of co-investments in the portfolio.

Capital activity timing adds another layer of difficulty. Capital calls do not follow a predictable schedule. A GP may issue a call with ten business days’ notice, and the family office needs to fund it from available liquidity. Distributions arrive on their own timeline, sometimes with minimal advance detail on the breakdown. For offices managing cash across multiple co-investments and fund commitments simultaneously, the lack of consistency in timing and format makes cash forecasting an active planning exercise rather than something that falls out of a report. Quarter-end and year-end close processes are particularly vulnerable, because late-arriving documents can force restatements or hold up deliverables.

Entity and ownership structures compound the problem. A single co-investment might be held through a special purpose vehicle, with the family office’s interest sitting inside a holding entity that also owns stakes in other investments. Posting a capital call correctly means understanding which entity received the call, how the economics flow through the ownership chain, and where the entry lands in the general ledger and the partnership accounting records. Allocation work increases with every additional layer, and so does the reconciliation effort when something does not tie.

All of this has to hold up under audit. Auditors do not accept a number in a spreadsheet without being able to trace it back to a source document. That means the back office needs to maintain a clear, retrievable link between every posted entry and the GP notice or statement it came from. When the source documents are scattered across portals, email folders, and shared drives, and when the data has been manually rekeyed into a system, maintaining that link is its own workstream. Teams end up building binders, cross-reference logs, and folder structures whose only purpose is proving that the numbers in the books came from somewhere real.

The cumulative effect is that co-investments, which may represent a relatively small number of positions in the portfolio, consume a disproportionate share of operational effort. The work is not analytical. It is extractive, repetitive, and high-stakes in the sense that errors show up in reporting and audit, where they are most expensive to fix.

What Document Intelligence changes

FundCount’s AI Document Intelligence, referred to here as DI, is designed to sit between the inbound document stream and the accounting and reporting system. Its job is to take the unstructured GP documents that drive co-investment operations and convert them into structured, reviewable data that can be posted into FundCount’s integrated workflows.

As of this writing, FundCount is the only platform that combines AI-based document extraction for co-investment documents with integrated portfolio accounting, partnership accounting, and general ledger workflows in a single system.

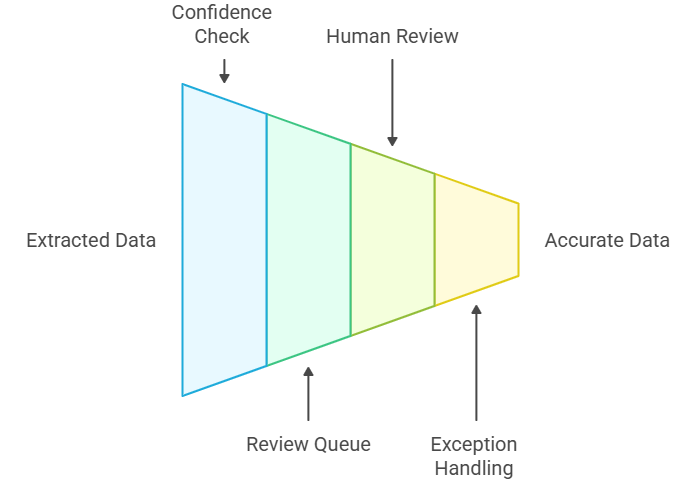

At a functional level, DI ingests the documents a family office back office already receives. Capital call notices, distribution notices, capital account statements, quarterly reports, K-1s, and co-investment financial statements. It reads each document using large language model-based extraction rather than relying on fixed templates or traditional OCR, which means it can handle the format variation that makes co-investment documents difficult to process at scale. From each document, DI identifies and extracts the relevant fields and tables, including amounts, dates, entity identifiers, fee breakdowns, and line-item detail. It then normalizes what it finds into a consistent structure so that a capital call from one GP lands in the same format as a capital call from another, regardless of how the original notice was laid out.

Where DI differs from a pure extraction tool is in how it handles uncertainty. Rather than pushing every result straight into the books, DI flags data points that fall below a confidence threshold and routes them into a review queue. The back office team sees what was extracted, where it came from in the source document, and why the system is asking for a second look. This means exceptions get caught before they become posting errors, and the review process is focused on the items that actually need human judgment rather than spread across every line of every document.

For co-investment workflows specifically, this changes the shape of the work. The hours that previously went into reading each PDF, rekeying figures into spreadsheets or accounting software, and cross-checking entries against source documents get compressed into a review-and-approve cycle. Data moves from ingestion into FundCount’s portfolio accounting, partnership accounting, and general ledger without requiring a separate extraction vendor or a manual bridge between systems. Because the original documents remain accessible from within the platform and are linked to the data they produced, the audit trail is built into the process rather than reconstructed after the fact.

The practical result is that a growing co-investment program does not have to scale its back office headcount in proportion to its document volume. The volume still exists, but the operational cost of converting that volume into clean, posted, auditable data drops significantly when the extraction, normalization, and review steps are handled inside the same system that maintains the books.

How FundCount supports co-investment operations end to end

DI handles the first stage of the workflow, getting from a raw document to transaction-ready data. But the value of having extraction built into FundCount rather than bolted on through a separate vendor is what happens after that stage. Once data has been extracted, normalized, and reviewed, it is already inside the system that maintains the books.

Capital calls and distributions are the most frequent co-investment transactions, and they are also the ones most sensitive to timing and accuracy. When a capital call notice is processed through DI, the extracted data, including the call amount, due date, entity, and any fee or expense detail, can be reviewed and posted into FundCount’s partnership accounting and general ledger without re-entry. The same applies to distribution notices, where the breakdown between return of capital, realized gains, and income needs to land correctly for both reporting and tax purposes. Handling these inside one system means the data that drives cash planning, the data that hits the books, and the data that appears in reporting all originate from the same reviewed extraction.

Position and cost basis tracking follows naturally. Each posted transaction updates the investment record, so the family office has a current view of its cost basis, unfunded commitments, and ownership percentages across all co-investments. This is particularly useful when a single family office holds co-investments through multiple entities or alongside fund commitments with the same GP, because FundCount’s accounting structure can reflect the full ownership chain rather than flattening it into a summary.

Performance and exposure reporting is where the integrated model pays off most visibly. Family offices that hold a mix of fund interests, direct investments, and co-investments need to see performance across all three. They also need to slice exposure by manager, sector, geography, strategy, or whatever dimensions their investment committee and advisors require. Because FundCount holds the accounting records, the portfolio data, and the source documents in one platform, these views can be built from the same data set rather than assembled from separate systems and reconciled manually.

Audit support ties the whole workflow together. Every extracted data point links back to the source document it came from, and those documents remain accessible from within FundCount. When an auditor asks to see the notice behind a capital call posting, the back office can surface it directly from the system rather than searching through email archives or portal downloads. That traceability is built into the normal course of processing, which means audit preparation becomes a retrieval exercise rather than a reconstruction project.

What a good operating model looks like

Technology solves the extraction and integration problem, but a co-investment program still needs operational discipline around how the data flows and who is responsible for what.

A few practical controls make the difference between a program that scales cleanly and one that accumulates exceptions.

First, every document processed through DI should go through a standard review step before posting. DI flags items that need attention, but the back office should also have its own checklist for verifying key fields against prior period data, confirming entity mapping, and validating that fee and expense allocations match the terms of the co-investment agreement. Exception handling should follow a defined path, with clear escalation when something does not reconcile, rather than getting resolved informally in someone’s inbox.

Second, data ownership between the investment team and the back office needs to be explicit. The investment team typically owns the relationship with the GP and has context on deal terms, expected capital activity, and any amendments. The back office owns the posted data, the reporting, and the audit file. When those responsibilities blur, documents sit in limbo, and quarter-end timelines slip. A simple handoff protocol, covering when documents are expected, who is responsible for getting them into the system, and who reviews the output, prevents most of the coordination failures that slow down close processes.

Third, new GP formats should be handled through a documented mapping approach rather than figured out ad hoc each time. When a family office adds a new co-investment with a GP it has not worked with before, someone needs to review how that GP’s documents are structured, confirm that DI is extracting the right fields, and verify that the data maps correctly into FundCount’s accounting and reporting framework. Doing this once per GP and recording the result means the second and third document from that manager flows through without the same startup cost.

On scalability, this is the operating model that allows a family office to grow its co-investment program without growing its back office in proportion. Adding a new co-investment adds document volume, but if the extraction, review, and posting workflow is already functioning, the incremental effort per deal decreases. BNY Wealth’s 2025 study flagged understaffing as a constraint on direct investing programs, and the pattern described here is a direct response to that constraint. The goal is a process where the tenth co-investment is operationally lighter than the first, because the infrastructure and controls are already in place.

Conclusion

Co-investments are a sound way for family offices to deploy capital. The operational challenge is not the investment itself but the recurring cost of converting unstructured GP documents into clean, posted, auditable data. That cost is where most programs lose time and where errors are most likely to surface.

One useful benchmark is to estimate how many hours per month your back office spends reading co-investment documents, rekeying figures into spreadsheets or accounting software, and reconciling the results before reporting or audit. If that number is growing alongside your deal count, the process is scaling in the wrong direction.

FundCount built Document Intelligence to change that trajectory. If you want to see what it looks like in practice, we can walk through a real co-investment document package, from GP notice to posted transaction to reporting output, using your actual document types and workflows.