If you’ve attended a wealth management conference in the past two years, you’ve probably heard the phrase “AI-powered” applied to nearly everything. AI-powered portfolio analysis. AI-powered risk detection. AI-powered client onboarding. At some point, you half expect someone to announce an AI-powered coffee machine in the breakout room.

The enthusiasm is understandable. Artificial intelligence has made genuine progress in areas that matter to family offices and wealth managers, from automating tedious data entry to identifying patterns across large datasets that would take a human team weeks to spot. These are real capabilities with real operational value.

But somewhere between the genuine advances and the marketing copy, the conversation has gotten a little loose. AI has become one of those terms that gets attached to products and strategies without much explanation of what it actually does, how it works, or what it needs in order to work well. And that last part tends to get the least attention, even though it may be the most important.

Because here’s what rarely makes it into the keynote slides. AI in wealth management is almost entirely dependent on the quality of the data underneath it. The most sophisticated algorithm in the world will produce unreliable outputs if it’s drawing from fragmented, inconsistent, or poorly maintained data. And for many firms, that’s exactly the situation they’re in.

This article takes a balanced look at where AI stands today in the wealth management space, what it can genuinely help with, and what needs to be true about your data infrastructure before any of it matters.

AI in Family Offices

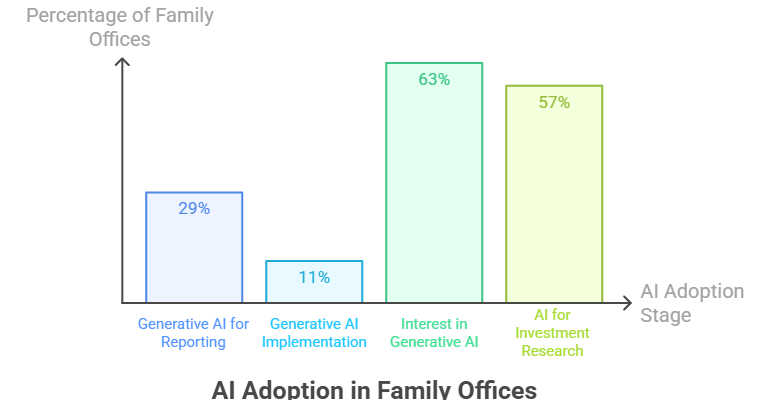

It would be hard to find a wealth tech trends report from the past two years that doesn’t feature AI prominently. And the data shows that the interest is genuine. According to the 2025 North America Family Office Report from RBC and Campden Wealth, 29% of family offices now use generative AI for investment reporting, up from just 11% that had implemented it in any form the year before. Another 63% expressed interest in adopting it. The Bank of America 2025 Family Office Study found that 57% of family offices are already using AI for aspects of investment research, with adoption climbing alongside assets under management.

So the momentum is real. But the way AI gets discussed in the industry often skips over important details. Vendor marketing tends to focus on outcomes. Faster reporting. Smarter analysis. Fewer errors. What it rarely addresses is the set of conditions that need to be true before any of those outcomes become possible. And for many family offices, those conditions aren’t met yet.

The most commonly cited operational risk among family offices today, according to the same RBC/Campden report, is manual processes and over-reliance on spreadsheets. That finding is revealing. It means a significant portion of the industry is still managing critical workflows through fragmented, manually maintained systems. Layering AI on top of that kind of environment doesn’t accelerate insight. It accelerates confusion. The outputs of any AI tool are shaped entirely by the inputs it receives, and when those inputs are inconsistent, siloed, or riddled with gaps, the results will reflect that.

This is the tension at the center of the AI conversation in wealth management. The technology is advancing quickly, and many of the use cases are legitimate. AI can extract structured data from messy PDF statements. It can flag anomalies across large transaction sets. It can reduce hours of manual reconciliation work. FundCount’s AI Document Intelligence, for example, uses large language models to pull book and tax data from alternative investment statements of varying formats, feeding structured output directly into accounting workflows. These are practical, measurable gains.

But they work because the data pipeline underneath is sound. The extraction layer connects to a unified general ledger. The outputs flow into a system that was already designed to maintain accuracy across entities, asset classes, and currencies. Without that foundation, the same AI tool would be producing structured data with nowhere reliable to go.

The gap between AI’s promise and its practical value in family offices almost always comes down to data quality. And until more firms address that gap, the industry will continue to see a split between offices where AI is genuinely useful and offices where it’s mostly decorative.

What AI in family offices can actually do right now

It’s easy to get lost in the big claims, so it helps to ground the conversation in what’s already working. The practical applications of AI in family offices today tend to be less glamorous than the marketing suggests, but they’re genuinely useful. And in many cases, they’re solving problems that have frustrated operations teams for years.

Document extraction and data entry automation

This is probably the most immediately impactful use case. Family offices regularly receive statements from fund managers, custodians, and banks in a wide range of formats. Capital call notices, distribution statements, NAV reports. Many of these arrive as PDFs with inconsistent layouts, and historically, someone on the team has had to manually key that data into the accounting system. AI-powered document intelligence can now read those documents, interpret their structure, and extract the relevant fields automatically. FundCount’s AI Document Intelligence does exactly this, using large language models to pull book and tax data from alternative investment statements and feed it directly into the accounting workflow. Unlike older OCR-based tools that broke whenever a fund manager changed their statement format, LLM-driven extraction can handle layout variations without requiring new templates or retraining.

Anomaly detection

AI is well suited to scanning large volumes of transaction data and flagging entries that fall outside expected patterns. A duplicate invoice, an unusually large fee, a transaction booked to the wrong entity. These are the kinds of errors that a human reviewer might catch on a good day but miss under time pressure, especially during month-end close. According to Accenture, as much as 80% of routine accounting tasks can be automated, and Deloitte has credited AI adoption with cutting the time staff spend on certain tasks in half. For family offices managing complex, multi-entity structures, even catching one misbooked entry before it flows into downstream reports can prevent hours of reconciliation work.

Research synthesis and summarization

The 2025 Bank of America Family Office Study found that 57% of family offices are already using AI for aspects of investment research. In practice, this often looks like using generative AI to summarize lengthy fund manager reports, scan news feeds for relevant developments, or condense due diligence materials into briefing documents. It’s not making investment decisions. It’s compressing the time it takes for a human to get informed enough to make one. JPMorgan’s research echoes this, finding that nearly 80% of ultra-high-net-worth principals use AI in their personal lives, with 69% also using it within their businesses.

Reconciliation support

Matching records across custodians, banks, and internal ledgers is one of the most time-intensive tasks in family office operations. AI tools can accelerate this by identifying probable matches, flagging discrepancies, and learning over time which exceptions are routine versus which ones require attention. This doesn’t eliminate the need for human review, but it dramatically reduces the volume of items a person needs to look at manually.

What ties all of these use cases together is that they sit in the operational layer of a family office. They help teams process information faster and with fewer errors. They don’t replace judgment, and they don’t generate investment alpha on their own. But for firms that have spent years wrestling with manual data entry, inconsistent statements, and slow reconciliation cycles, these are meaningful improvements.

The important caveat, and one that the next section will dig into, is that every one of these applications depends on data quality AI can actually work with. An anomaly detection tool can’t flag what’s wrong if it doesn’t have a reliable baseline for what’s right. An extraction engine is only useful if the data it produces flows into a system that can maintain it accurately. The technology is ready. The question is whether the data infrastructure behind it is too.

What’s still science fiction

For every realistic AI use case in wealth management, there’s a counterpart that gets talked about as though it’s just around the corner when it’s really still years away. Being honest about that gap matters, because firms that invest based on inflated expectations tend to end up disappointed, and sometimes worse off than if they’d done nothing at all.

The fully autonomous portfolio manager

This is the one that gets the most airtime. The idea that an AI system could independently analyze markets, assess risk, rebalance portfolios, and execute trades across a complex, multi-entity family office structure without meaningful human involvement. It makes for a compelling conference panel, but the reality is far more constrained. AI can support portfolio analysis and flag areas that deserve attention. It can model scenarios and surface correlations in historical data. But managing a family’s wealth involves context that no model currently captures well. Tax implications across jurisdictions, family governance preferences, liquidity needs tied to lifestyle or business obligations, relationships with co-investors. These are judgment calls that require experience, conversation, and an understanding of the client’s full picture.

Predictive market intelligence

There’s a version of this pitch where AI “sees” market movements before they happen. Some tools do use machine learning to identify patterns in historical market data, and a handful of quantitative funds have built strategies around this. But for the typical family office, the idea that an AI tool will reliably predict what’s coming next in the market is misleading. Markets are shaped by human behavior, geopolitical events, and policy decisions that frequently defy historical patterns. AI can help organize and interpret information faster, but treating it as a crystal ball is a recipe for overconfidence.

Plug-and-play AI transformation

Perhaps the most quietly damaging myth is the idea that a firm can simply “add AI” to its existing setup and see immediate, transformative results. Vendors sometimes encourage this perception by positioning their tools as turnkey solutions. In practice, AI adoption that actually delivers value requires preparation. It requires clean, structured data. It requires systems that can receive and act on the outputs. And it requires people who understand what the tool is doing well enough to evaluate whether the outputs make sense. The 2025 RBC/Campden Wealth report found that the most commonly cited operational risk among family offices is still manual processes and spreadsheet dependency. For firms in that position, the path to useful AI runs through infrastructure improvement first.

AI-driven client relationship management

Some wealth tech trends coverage has floated the idea of AI systems that can independently manage client communications, anticipate client needs, and personalize interactions without advisor involvement. While AI can help draft correspondence, summarize meeting notes, or flag when a client hasn’t been contacted in a while, the relationship itself remains fundamentally human. High-net-worth clients expect to speak with someone who knows them. They want judgment, empathy, and accountability from a person, not a language model. AI can support the advisor in being more prepared and responsive, but it can’t stand in for the relationship.

None of this is meant to dismiss the trajectory of the technology. AI capabilities are advancing quickly, and some of what seems impractical today may become feasible within a few years. But for family offices making decisions right now about where to invest their time and budget, the distinction between what works today and what remains aspirational is worth drawing clearly. The firms getting the most value from AI are the ones treating it as a tool for specific operational problems, not as a strategy in itself.

The data quality problem behind AI in family offices

There’s a pattern that plays out regularly when family offices begin exploring AI tools. The initial excitement is high. The demos look impressive. The vendor promises faster reconciliation, smarter reporting, fewer errors. Then the firm starts implementation and runs into a wall that has nothing to do with the technology itself. The data isn’t ready.

This shouldn’t be surprising, but it catches a lot of firms off guard. AI tools are pattern-recognition engines at their core. They learn from data, make decisions based on data, and produce outputs shaped entirely by the data they receive. When that data is clean, consistent, and well-structured, the results can be remarkable. When it’s not, the outputs range from unreliable to actively misleading.

For many family offices, the data environment has evolved organically over years. Holdings are tracked in one system, partnership accounting in another, bank data in spreadsheets, and alternative investment statements in email attachments. Each of these sources may be accurate in isolation, but they rarely speak the same language. Field names differ. Formats are inconsistent. Timing varies. And the task of reconciling everything into a unified picture has traditionally fallen to a small team doing manual work on a deadline.

Layering AI on top of that kind of environment creates a specific risk. The tool will still produce outputs. It will still generate reports, flag anomalies, and extract data. But without a reliable baseline of clean, unified data, those outputs may reflect the inconsistencies of the inputs rather than anything meaningful about the portfolio. An anomaly detection model trained on messy data will learn the mess as normal and miss the actual exceptions. An extraction tool feeding data into a fragmented system will simply create well-formatted entries in the wrong places.

The RBC/Campden Wealth 2025 report is revealing on this point. When family offices were asked about their top operational risks, the most common answer wasn’t cybersecurity or regulatory change. It was manual processes and spreadsheet dependency. And the most sought-after technology, cited by 27% of respondents, wasn’t an AI product at all. It was wealth aggregation platforms and automated reporting systems that consolidate data from multiple financial institutions into a single view. In other words, the industry’s most pressing technology need is the foundational layer that makes AI useful in the first place.

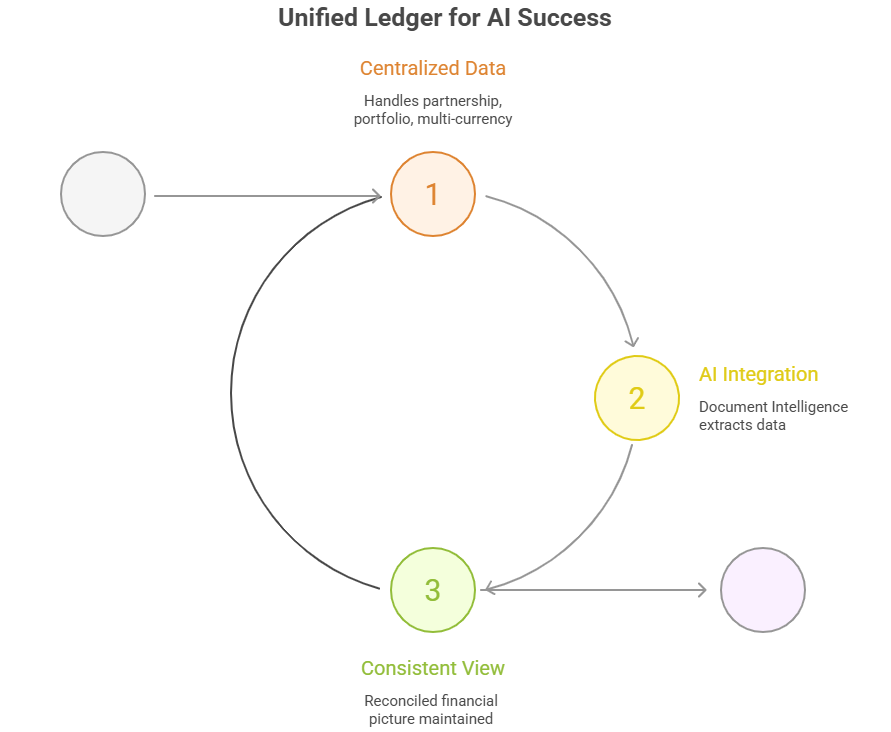

FundCount’s approach to this problem is worth noting because it addresses the sequence directly. Rather than bolting AI onto a patchwork of disconnected systems, FundCount operates on a unified general ledger that handles partnership accounting, portfolio data, and multi-currency financials in one place. When AI tools like its Document Intelligence module extract data from fund manager statements, that data flows into a system that already maintains a consistent, reconciled view of the client’s financial picture. The quality of the AI output is protected by the quality of the system it feeds into.

This is the part of the AI conversation that tends to get the least attention, precisely because it’s less exciting than talking about algorithms and automation. But for any family office serious about putting AI to work, data quality isn’t a prerequisite to check off and forget. It’s the ongoing condition that determines whether the technology delivers value or just adds another layer of complexity.

Clean data and unified systems come first

If there’s one takeaway from the data quality discussion, it’s that AI readiness isn’t really about AI. It’s about whether the systems underneath are structured well enough to support it.

For family offices, this comes down to a few practical questions. Is the firm’s financial data consolidated in a single system, or is it scattered across multiple platforms, spreadsheets, and email inboxes? When someone needs a full picture of a client’s holdings across entities, asset classes, and currencies, can they pull it from one place? And when new data comes in from custodians, banks, or fund managers, does it flow into the system automatically, or does someone have to reformat and rekey it?

The firms that can answer those questions favorably are the ones positioned to get real value from AI. Everyone else is likely to spend more time cleaning up after AI tools than benefiting from them.

This is where the concept of a unified general ledger becomes relevant beyond the accounting team. A platform like FundCount was built around the idea that partnership data, portfolio data, and entity-level financials should all live in the same system, governed by the same logic and updated through automated data feeds. That kind of architecture does more than simplify reporting. It creates the conditions where AI can function reliably, because the data it touches has already been reconciled, standardized, and validated before any model ever sees it.

The industry data supports this priority. The 2025 RBC/Campden Wealth report showed that 69% of family offices have now adopted automated investment reporting systems, up from 46% the year before. That’s a significant jump, and it suggests that firms are recognizing the operational cost of maintaining fragmented, manually driven workflows. For many, the motivation isn’t even AI specifically. It’s the basic need to produce accurate, timely reporting without burning through staff hours on data wrangling. AI becomes a natural next step once that foundation is in place, not a substitute for building it.

It’s also worth noting that clean data and unified systems have value independent of any AI application. They reduce the risk of errors in client reporting. They make audits less painful. They allow the team to respond to ad hoc client requests without scrambling to pull data from five different sources. And they make onboarding new staff far easier, because the institutional knowledge isn’t trapped in someone’s personal spreadsheet. AI amplifies these benefits, but the benefits exist even without it.

The firms that approach this the other way around, buying the AI tool first and hoping to sort out the data later, tend to end up with expensive software that nobody trusts. And in a family office, where the team is small and every hour counts, that kind of misstep is hard to recover from.

Approaching AI with curiosity and healthy skepticism

The wealth management industry has a long history of technology hype cycles. Cloud computing, blockchain, robo-advisory. Each was introduced with sweeping predictions about how it would transform everything, and each eventually found its place as a useful tool within a broader ecosystem rather than the revolution it was billed as. AI is following a similar trajectory, though the practical applications may turn out to be broader and more durable than some of its predecessors.

The healthiest approach for family offices right now is to stay genuinely curious about what AI can do while remaining clear-eyed about what it can’t. That means evaluating tools based on the specific operational problems they solve rather than on how impressive the demo looks. It means asking vendors hard questions about what happens when the data is messy, incomplete, or formatted inconsistently. And it means being honest internally about whether the firm’s data infrastructure is actually ready to support the tools being considered.

It also means resisting the pressure to adopt AI simply because competitors are talking about it. The BNY Wealth 2025 study found that 83% of family offices rank AI as a top conviction theme for the next five years. That’s a remarkable level of interest, and it reflects genuine potential. But interest and readiness are different things. A firm that takes six months to clean up its data environment, consolidate its systems, and implement automated feeds before introducing AI will almost certainly get better results than one that rushes to deploy a model on top of a fragmented foundation.

The family offices getting the most from AI today share a few common traits. They started with a clear, bounded problem rather than a sweeping transformation initiative. They made sure their accounting and reporting systems were unified before layering on intelligent tools. And they treated AI as something that enhances the work their team already does rather than something that replaces the need for skilled people. FundCount’s own trajectory reflects this thinking. Its AI Document Intelligence module works precisely because it connects to an accounting platform that was already built for accuracy, consolidation, and multi-entity complexity. The AI makes the system faster. The system makes the AI trustworthy.

For wealth managers and family offices still deciding where to start, the honest answer is probably not with AI at all. It’s with the data. Get that right, and AI becomes a natural, productive addition to the operation. Skip that step, and even the most sophisticated tools will struggle to deliver on their promise.