A family office can run for years on QuickBooks, Sage, NetSuite, Excel, custodian portals, portfolio reporting tools, and PDFs from private managers. The pricing question usually appears when that stack starts to cost too much in manual reconciliation, delayed reporting, and key-person dependency.

The family office software cost conversation is not only about the annual subscription. It is about whether the price matches the office’s operating complexity: entities, users, asset classes, data feeds, report packs, hosting, integrations, implementation, and support.

This article explains what drives cost, why quotes vary, and how to compare family office software pricing without reducing the decision to one headline number.

Decision summary

| Question | Practical answer |

| What drives family office software cost? | The largest drivers are usually entity complexity, number of users, data sources, asset classes, report customization, implementation scope, hosting or deployment needs, integrations, and support model. |

| Why do quotes vary so much? | Two offices with the same AUM can have very different structures. A 5-entity office with simple reports is not the same project as a 40-entity office with trusts, partnerships, alternatives, custom report packs, and multiple data feeds. |

| What is easy to compare? | Published starting prices, included users or package limits, hosting assumptions, training approach, and whether implementation is scoped separately. |

| What is harder to compare? | Custom reports, historical migration, data-feed coverage, security requirements, integration work, exception workflows, and how much manual work remains outside the system. |

| What should buyers ask for? | Ask vendors to separate software subscription, implementation services, hosting or deployment, data feeds, custom reports, integrations, training, and support. |

Family office software costs more when systems stay disconnected

FundCount helps reduce operational complexity by bringing accounting, reporting, and consolidation into one platform.

What drives the cost of family office software

The price of software rarely reflects one variable. For a family office, the quote usually reflects both the software package and the work required to make that software fit the office’s real operating model.

A basic accounting setup might have a small number of entities, one chart of accounts, a limited report pack, and a few users. A more complex office may need multi-entity accounting, public and private investment accounting, custodian and broker feeds, partnership accounting, multi-currency reporting, custom statements, and downstream exports for advisors or tax teams.

That is why a useful pricing conversation starts with scope, not just software category.

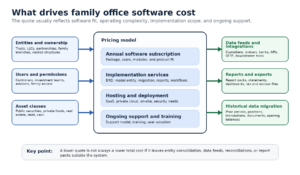

Diagram: Core variables that affect family office software cost.

The most important cost drivers fall into 8 groups.

1. Entities and ownership structures

Entity count matters, but structure matters more. A family office with 10 flat entities may be easier to implement than one with fewer entities but complex trust ownership, related-party activity, intercompany loans, or nested investment vehicles.

Pricing and implementation scope often change when the software needs to support entity-level books, consolidated reporting, look-through ownership, family member views, and allocation rules.

2. Users, roles, and permissions

Software cost may change based on the number and type of users. A controller who posts journals, an investment team member who reviews positions, an advisor who needs read-only access, and a principal who receives reports do not all need the same permissions.

Before comparing quotes, define who needs access, what each user needs to do, and whether family members or outside advisors will use a portal or receive exported reports.

3. Asset classes and accounting complexity

Public securities, bank cash, and operating expenses are different from private equity, real estate, loans, derivatives, side pockets, capital calls, distributions, and partnership allocations.

The more the office needs portfolio accounting, partnership accounting, and investment activity connected to the general ledger, the more important it becomes to validate the software against actual transactions and reports.

4. Data feeds and source coverage

Data feeds can reduce manual downloads, but they also add scope. The office needs to know which custodians, brokers, banks, market data providers, and alternative managers are in the first phase.

For data aggregation for family offices, the question is not just whether data can be imported. It is whether holdings, transactions, cash, prices, FX rates, and private investment data can be mapped, reconciled, reviewed, and reported from the same operating layer.

5. Reporting and report-pack customization

Reporting is one of the biggest sources of pricing confusion. One vendor may include standard templates, while another may quote custom report work separately. A family office may also need reports to match a current format rather than simply produce a similar view.

If the office needs entity-level balance sheets, consolidated net worth reports, capital statements, performance reports, tax-supporting schedules, dashboards, and advisor exports, reporting scope should be explicit before comparing prices for family office reporting software.

6. Historical migration

Historical migration can be small or large depending on what the office needs to bring forward. Opening balances and current positions are very different from years of transaction history, capital activity, private investment documents, prior NAVs, realized gain details, and legacy report logic.

A shorter migration can reduce implementation cost, but it may limit historical analysis. A longer migration may support better reporting continuity, but it requires more validation.

7. Hosting, deployment, and security requirements

Some offices are comfortable with a managed cloud setup. Others require private cloud, on-site deployment, isolated databases, specific backup expectations, or deeper security review.

Hosting and deployment choices affect both price and timeline. They should be discussed with security, legal, operations, and finance stakeholders before the quote is treated as final.

8. Integrations, exports, training, and support

Many offices still need CRM tools, document management, payroll, tax tools, BI dashboards, or a data warehouse. That means pricing should include the cost of exports, APIs, file imports, or other integration work that keeps those systems connected.

Training and support also matter. If users do not know how to review exceptions, validate reports, or manage workflows, the office may keep relying on the same spreadsheets it was trying to reduce.

Family office accounting software pricing: why quotes vary by complexity

Family office accounting software pricing varies because family offices rarely share the same operating model. A quote based on AUM alone can be misleading if it ignores entities, asset classes, data sources, and reporting needs.

| Pricing variable | Why it changes cost | What to clarify before comparing quotes |

| Entities and ownership | More entities, nested ownership, trusts, LLCs, partnerships, and family branches can require more setup and reporting logic. | How many entities need books, reporting, consolidation, or look-through views? |

| Users and permissions | Different user roles require different access rights, approvals, and training. | Who posts, reviews, approves, exports, and receives reports? |

| Asset classes | Private investments, loans, derivatives, real estate, and partnership structures require more accounting detail than simple public securities. | Which asset classes must be live in phase 1? |

| Data feeds | Custodian, broker, bank, market data, and alternative investment sources may require mapping and validation. | Which sources are connected, imported, or handled manually? |

| Reports and exports | Custom report packs, portal outputs, tax schedules, and advisor files can expand scope. | Which reports must match current formats exactly? |

| Historical migration | More periods and more transaction detail require more review. | What history is necessary for go-live versus later phases? |

| Hosting and security | Deployment model, backups, security review, and data-control needs can affect price. | What deployment model and security documentation are required? |

| Support and training | More teams and workflows require more enablement. | What training is needed for accounting, investment, operations, and reporting users? |

The practical lesson is simple: compare quotes by workflow coverage, not just subscription price. A lower-cost system may still be expensive if the team keeps reconciling QuickBooks, Excel, custodian files, and portfolio reports outside the system.

Published FundCount pricing examples

FundCount publishes starting prices for several packages. These numbers should be treated as starting points, not final quotes, because implementation scope, hosting, data feeds, users, and reporting requirements may change the total cost.

The HNW and Small Family Office package starts from $24,000 per year and is listed for organizations with up to 15 entities, 50 investors, 500 positions, and US$30 million in assets under management. The public page describes this offer as investment accounting and reporting delivered as a service, with hosting, support, software operation, and reconciliation service included.

The Single Family Office package starts from $34,099 per year, with digital transformation and hosting fees applying. The page describes support for custodians, brokers, banks, alternative managers, reconciliations, full financials, and data feeds across family entities.

The Multi-Family Office package starts from $24,449 per year, with digital transformation and hosting fees applying. The public page describes reporting for each family, data-feed automation, custodian and broker integration, investment, partnership, and general ledger capabilities, and privacy and data security across families.

FundCount also lists a Sandbox option at $899 per month, available for one month, for experienced investment system users who want to assess a fully functional web application.

Because pricing pages can change, use the published numbers as the current public baseline and confirm package fit during evaluation.

One platform can simplify the family office stack

FundCount combines accounting, reporting, and multi-entity consolidation to reduce operational overhead.

Why the current stack can hide the real cost

QuickBooks, Sage, NetSuite, Excel, Addepar, Black Diamond, Arch, Power BI, Snowflake, tax tools, and custodian portals can each serve a useful role. The cost problem starts when every month requires a manual handoff between those systems.

A spreadsheet may look inexpensive until it becomes the place where the team stores transaction adjustments, entity mappings, capital account logic, valuation notes, report formulas, and approval comments. A portfolio reporting platform may be valuable for investment visibility, but the office still needs to decide what system owns accounting truth. A general ledger may handle basic books, while investment activity, private assets, and family reports still require workarounds.

That hidden cost should be part of the buying case. The office should count the time spent downloading files, reconciling differences, rebuilding reports, checking formulas, fixing formatting, answering follow-up questions, and explaining why two systems do not match.

How to reduce pricing and implementation risk

Pricing gets clearer when the office turns the evaluation into a scope exercise. The goal is not to make implementation sound simple. The goal is to identify complexity early so the quote reflects the work required.

Diagram: A phased path from rough pricing to validated implementation scope.

A practical evaluation process should include:

- an entity chart, including trusts, LLCs, partnerships, individuals, foundations, and related vehicles;

- a list of users and required permissions;

- current report packs and examples of required formats;

- the list of custodians, brokers, banks, data providers, and alternative managers;

- the current GL, portfolio reporting tool, data warehouse, CRM, and document tools;

- required exports for tax, advisors, BI, or internal models;

- historical migration requirements;

- hosting, security, backup, and legal review needs;

- and success criteria for the first live reporting cycle.

FundCount’s implementation process includes a business analysis phase that produces a Business Requirements Document covering custom workflows, functionality, and reporting requirements. FundCount’s public implementation page also describes a gate decision before software deployment, an execution phase that starts with one entity, later milestones for all entities and data links, and training for team members.

That staged process is important because it separates a sales estimate from an implementation scope. Buyers should understand what is included, what is out of scope, and what needs validation before the first live reporting cycle.

Questions to ask vendors before comparing prices

Before choosing based on the lowest annual number, ask questions that expose the real operating cost.

- What is included in the annual subscription?

- What is billed separately for implementation?

- How many entities, users, accounts, positions, or investors are included?

- Which modules are included and which are optional?

- Which data feeds are supported today, and which require custom work?

- How are custodians, brokers, banks, alternative managers, and market data sources connected?

- Can the system reproduce current report packs, or only standard reports?

- How are custom reports priced?

- What historical data is migrated before go-live?

- What deployment and hosting options are available?

- What training is included?

- What support model applies after go-live?

- How are exports to tax, advisors, BI tools, or data warehouses handled?

- What assumptions would change the quote?

These questions make vendor comparisons more useful because they focus on the work the office actually needs to perform.

When a lower-cost option may be enough

A lighter tool may be enough if the office has a few entities, limited asset classes, simple reports, limited private investments, and a team that can reconcile source data quickly. In that case, the office may not need to pay for deeper investment accounting, partnership accounting, or complex reporting workflows yet.

A lower-cost option becomes riskier when the team still needs Excel to connect the books, investment activity, data feeds, entity ownership, and final reports. If the quote is low because the hardest work remains outside the system, the office should include that manual work in the cost comparison.

When purpose-built family office software is worth evaluating

A purpose-built family office platform becomes more relevant when the office needs accounting-backed reporting across entities, portfolios, partnerships, and data sources. FundCount is a fit when the problem is not only bookkeeping, but also investment accounting, data aggregation, reconciliation, entity-level reporting, consolidated reporting, and repeatable report production.

FundCount’s family office software page describes portfolio accounting, partnership accounting, general ledger, alternative investment document intelligence, reporting, investor portal, and data aggregation as part of the family office workflow. That product fit matters when the office wants source data, accounting records, and reporting outputs to connect in one operating layer rather than across disconnected spreadsheets.

Scenario guidance

If your office has simple bookkeeping, a small number of entities, and few investment workflows, start by improving the current process and keeping Excel limited to analysis rather than the system of record.

If your office is growing across entities, custodians, brokers, private investments, and custom report packs, compare vendors by how much manual reconciliation and reporting work remains after implementation.

If your office needs entity-level and consolidated reporting, capital statements, NAV, partnership allocations, custodian feeds, alternative investment data, and specific exports, evaluate family office accounting software pricing against the full cost of maintaining the current stack.

If your office is not ready for a full implementation decision, a sandbox or scoped workflow review can help test whether the software fits before the team commits to a broader migration.

FAQ

How much does family office software cost?

The answer depends on package fit, entities, users, asset classes, data feeds, reports, implementation scope, hosting, integrations, and support. Published starting prices help set a baseline, but the final quote should reflect the office’s actual operating requirements.

Why is implementation sometimes priced separately?

Implementation is often priced separately because no two family offices have the same entity structure, reporting requirements, data sources, migration history, or workflow needs. A scoped implementation helps define the work required before go-live.

Does AUM determine the price?

AUM may influence package fit for some offerings, but operational complexity often matters more. Entity count, ownership structures, private investments, reports, data feeds, and integrations can create more work than AUM alone suggests.

What should be included in a quote?

A useful quote should separate subscription, implementation, hosting or deployment, users, modules, data feeds, custom reports, migration, integrations, training, and support. It should also state assumptions that could change the final cost.

Can family offices keep QuickBooks, Sage, NetSuite, or Excel?

Yes, but the office should define each tool’s role. Excel can remain useful for analysis. General accounting systems may remain useful for basic books or AP. The risk appears when core investment accounting, entity ownership, reconciliations, and final report logic live across disconnected tools.

What should we prepare before asking for pricing?

Prepare an entity chart, user list, current report pack, data-source inventory, sample custodian or broker files, private investment statement examples, historical migration needs, required exports, hosting requirements, and a list of workflows that slow the team down today.

Conclusion

The right family office software cost is not the lowest quote. It is the price that matches the work the office needs the system to perform.

If the current stack can support accurate reports, quick reconciliation, clear ownership views, and controlled data movement, a lighter tool may be enough. If the team is still stitching together QuickBooks, Excel, custodian files, broker reports, private investment PDFs, and manual report packs, the cost comparison should include that ongoing work.

The next step is to turn pricing into a scope conversation: document your entities, users, data feeds, report packs, migration needs, hosting requirements, integrations, and support expectations. Then compare software based on what will be live, validated, and repeatable after implementation.